Our education system is designed to prepare generations to earn money and not to teach Money management or financial planning. In your life, you may meet some people who are not very serious about their financial planning. It is because they may not understand the financial risk. Even the younger generation never thinks about it and they start Financial Planning and investing very late in their life.

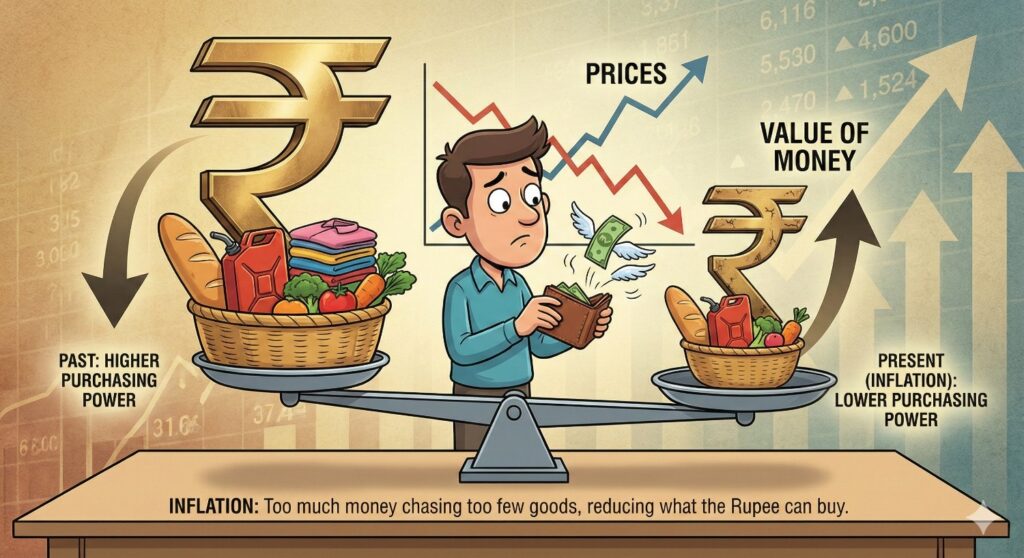

Inflation always reduces your purchasing power. Let’s have an example to understand, we all have a bank account and we keep our money in it as savings. Let’s assume you want to purchase an XYZ item and its price today is 1000 rs. But you’re planning to buy it next year. So you saved your 1000 rs in your bank account.

India’s inflation average for the last 10 years is 6.14. Now let’s do the calculation. Because of inflation after one year, you have to pay 1061 rs for the same item which was 1000 Rs last year. Otherside you kept your money in a bank account and the bank gave 4% interest on your 1000 which made 1040. A bank savings account gives roughly 3.5% to 4% interest on your savings. So if you understand, inflation reduces your money value by 21 Rs in terms of purchasing power.

If you want to learn how to beat inflation then you are at the right place.

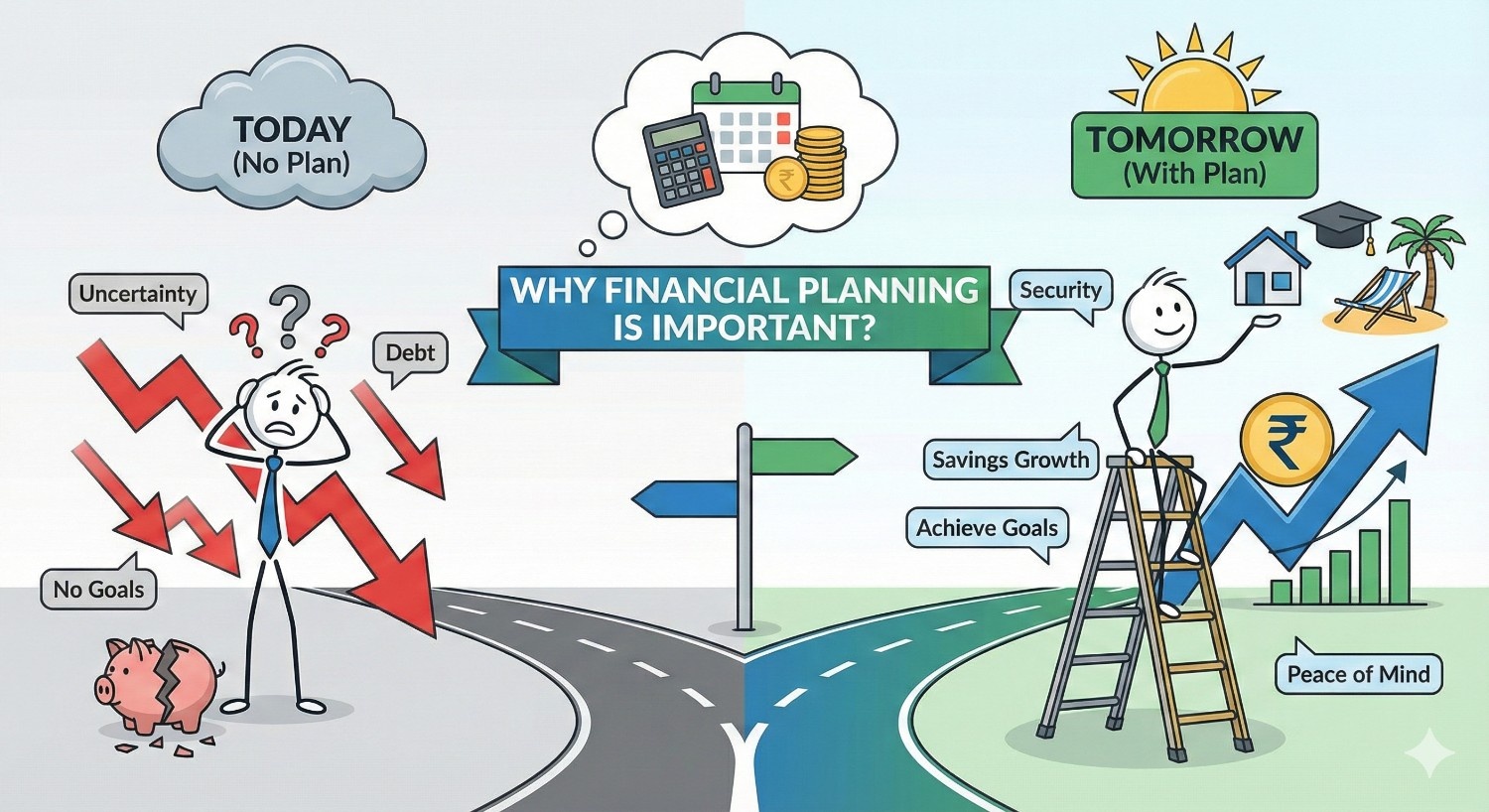

Why is Financial Planning important?

After discussing with people about their financial issues, I realised most of them think they are in financial problems because they are earning less or have loans or Medical Bills. But the real cause behind financial issues is the lack of financial knowledge, spending before saving, knowingly and unknowingly you spend more than your income etc.

So let’s understand why Financial Planning is important with a real-life example. I got to know about the story from the book “The Psychology of Money” by James Clear. Life story of two people. So let’s meet our characters with little information about them. The name of the first character in the story is “Mr. Ronal Read” who works as a gas station attendant, caretaker and machinic. He lives his life with hard work and a simple lifestyle. He owns a 2 bedroom house and spent his entire life there. He was the first High School graduate in his family. He struggled a lot in his childhood days.

Mr. Richard M. Fuscone, the second character of our story, was totally opposite to our first character “Mr. Ronal Read”. Richard was well educated. MBA from University of Chicago also attended Harvard Business School. He was one of top Wall Street executives and Merrill Lynch’s one-time head of Latin America. He owns an 18,000 square fit house and spends 80,000 dollars every month to maintain it.

Both were in the news but with different headlines. Mr. Ronal Read for charity, he donated 6 million dollars to the local hospital and library. On the other side, Mr. Richard Fuscone declared personal bankruptcy and sold his 18,000 sq.ft. house in foreclosure auctions. If you noticed both were totally opposite to each other, in their educations, jobs, pay and lifestyle but Mr. Ronal Read became a philanthropist and Mr. Richard Fuscone told the bankruptcy judge that “He does not have money.” What does this story tell us? Good jobs, big pay and education are meaningless if you do not know money management. Education or skill may help you to earn money, but that is not enough to stay wealthy. You will get many examples of people who earn good money but fail to stay wealthy. Let’s discuss how we can create wealth. I am sure after going through this blog you will understand better financially.

Build an Emergency Fund.

The emergency fund is the most important part of our journey. So what is an emergency fund and why is it so important? Emergency funds are your protector that will protect you from unplanned expenses like car or home repairs or from unavoidable emergencies like lost income or jobs, medical bills, etc. We all have somewhere experienced unexpected financial crises in our lives. Such crises are capable of pushing us into a debt trap or destroying our long term investment and future goals.

The latest example we faced was the Corona Virus crisis. People were forced to stay at home without pay. Many people lost their jobs. Corona makes us forced to think about saving and investing. The world was totally unaware when this pandemic would end. People used credit cards, breaking their investments to run houses. People were trapped in credit card debt or lost their savings and investments because they did not have any funds for such situations. Emergency funds will give you a stress-free life, protect your investment and give you time to recover from situations. Read more about the Emergency Fund.

Start Budgeting.

Budgeting is the 2nd most important step in our money management. Many people think budgeting is a complex, scary or boring process. It is a powerful tool that helps us to manage our every rupee. We can make sure how our money will be used. It will record where we spent our hard earned money. When you start budgeting, you may be surprised to see how much money we earned, saved, invested and spent on such things which were not even on our priority list. That money could be used to build an emergency fund or to reduce debt.

Budgeting will help us prioritize our requirements. We can arrange funds which we require every month like mobile or electricity bill, Home Rent or maintenance and yearly like health or life insurance premium, taxes, educations etc. It will make our life relaxing as budgeting helps us to understand our necessity and what we did for it. Budgeting will bring financial discipline to life. We will enjoy progress towards our financial goals.

Set Financial Goals

Financial goals are like milestones, when you reach them, you will feel like achievers and bring you closer to your future. Financial goals will also motivate you in your budgeting because both support each other. Financial goals must be achievable, realistic and aligned with your source of income. So before we set our goals, let’s understand three major categories:

- Long Term.

- Mid Term.

- Short Term.

Short Term Goals: The goals in this category can be achieved within a year. We can plan a new Apple Watch, television, Game console or small vacations or Dinner – Lunch, small academic courses etc. It is less important, even if you fail, life won’t change for the worse. So be ready to sacrifice some goals for Long Term or for Mid Term Goals.

Mid Term Goals: We can give more than a year and less than 3 years to achieve goals in this category. Goals in this category are a real challenge and very important. It may affect your budget or long term goals so give more focus, discipline and better budgeting for this category. Paying off debts, emergency funds for one year ( later we must extend up to 2 years ) and down payments for cars, big vacations etc.

Long Term Goals: We can assign more than 5 years for Long Term Goals. So comparably we have more time to adjust or re-align our financing or budgeting.

Investment plan

Investment planning is totally different from Financial Planning. Financial planning is a process to set direction to achieve goals and to deal with financial surprises. Investment Plan is like a guide for a financial vehicle, which drives money to financial goals. We need to put our money to work to generate income, wealth and reduce financial risk. As we all know without multiple sources of income, we can not become financially independent. So make your money work for you.

Let’s take an example to understand what an asset class and investment plan is. Suppose we saved some money and are planning to make an investment from it. So we will make a plan to decide how and what percentage will be allocated to the various investment classes ( Asset Class : Cash, Share Market, Mutual Funds, Real Estate, Bonds or various types of gold investment ) based on risk and returns. Before proceeding, we need to consider our goals, risk taking capacity and asset knowledge. Every asset performs differently so their risk and return will perform accordingly. Like keeping money in a savings account is more secure than investing in the share market. Saving Accounts give less returns and Stock Market investment can generate good returns with more risk comparatively to Saving Accounts.

Conclusion

Every one must learn money management along with their academic education. It is very important when you plan your future life and dreams. It will protect your money, time and peace of mind. You are not required to have any special skill to become an investor or financial planner just follow some basic rules as below:

- Start your investment early and regularly.

- Build emergency funds to protect your investments.

- Create and monitor your budget and investment plans.

- Always keep learning about investment and asset classes performance.

- Never invest all money in a single asset.

- Re-evaluate investment at least once in month based on risk, requirement, and asset performance.

- Stay invested for the long term. Wealth generated in long run.